Opening Speech by Mr. Justice John Hedigan, IBCB Chair

Good afternoon and welcome to this book launch event. We have at latest count some 200 attendees and a stellar cast of contributors. This is certainly a great tribute to our two learned authors. We have as guest speakers the Minister for Finance Paschal Donohue followed by Derville Rowland Director General, Financial Conduct of The Central Bank. We have then as panellists, Colin Hunt Chief Executive Officer of AIB and Mary O’Dea Chief Executive of The Institute of Banking. They will be joined in our panel discussion by our two authors. We welcome any questions that you may like to put in a Q and A and we will try to get to as many as possible.

The launch of a new book is always an occasion of joy and satisfaction in achievement and conclusion. I congratulate our two authors Joe McGrath and Ciaran Walker on this most timely of books, “New Accountability in Financial Services – Changing Individual Behaviour and Culture”. It follows “hot on the heels” of the publication on the 21st of July last by the government of The General Scheme of the Central Bank (Individual Accountability Framework) Bill 2021.

I am honoured to be asked and very pleased indeed to chair this launch event today. The proposed framework will be central to the developing culture of the financial services sector in Ireland. Thus, the Irish Banking Culture Board, of which I am chair, welcomes greatly this new initiative which will bring Ireland into line with other countries such as Australia, Hong Kong, Singapore, Malaysia and the United Kingdom. We together with our five member banks are strong supporters of an effective individual accountability framework incorporating a senior management accountability regime (SEAR) in Ireland similar to these other countries. The IBCB in March 2021 held a SEAR roundtable which considered aspects of this regime with international panellists. We have established a SEAR working group which met for the first time in May 2021 to discuss the proposed legislation from the perspective of the banking sector and to consider the lessons which can be learned from the experience of other countries in particular Australia and the United Kingdom. We in the IBCB look forward to contributing to the debate on the introduction of SEAR in Ireland. This is a priority area of focus for us in 2022 and onwards, in particular in relation to the proposed conduct standards within the accountability framework.

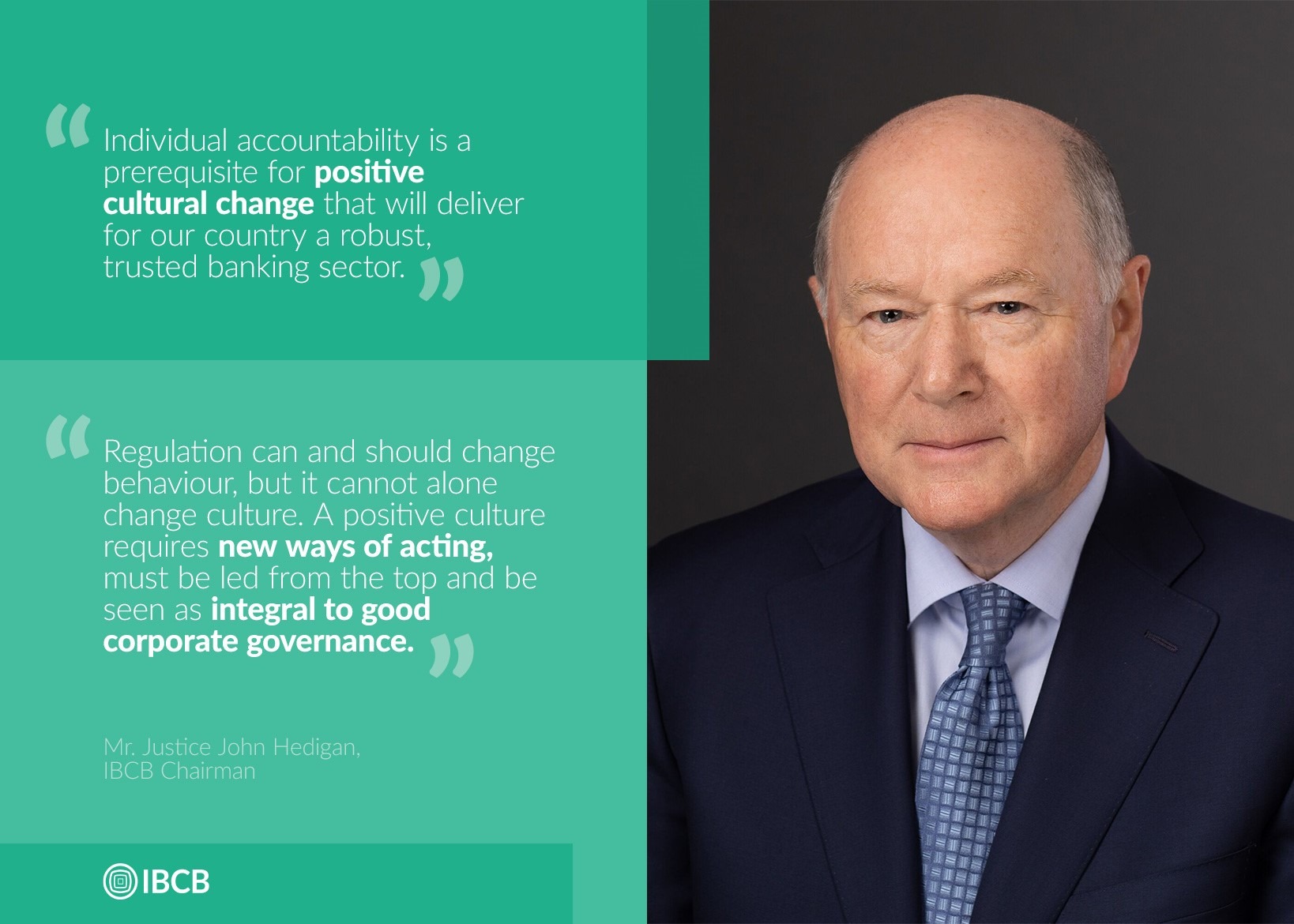

Our role in the IBCB is to work with our member banks and other stakeholders in the banking sector to enable the banks to build trustworthiness and thus regain the public trust. Lying at the very heart of this endeavour is the changing of individual behaviour and culture. Individual accountability is a prerequisite for positive cultural change that will deliver for our country a robust, trusted banking sector. This book is aimed squarely at that endeavour which has profound implications for the financial services sector including banks, for customers and for the wider community.

It seems to me that the learned authors proceed from the proposition that an interactive, cooperative approach between the regulator and the regulated entities is key to the success of the Individual Accountability Framework. They must work closely together. The authors demonstrate from the experience of the countries I mentioned above that this modus operandi, which places sanctions as a last resort, is a model that works best. This does not mean lighter or looser regulation. It means more effective regulation. The view is expressed however that focussing on individual and organisational factors alone is not enough. This is very much the IBCB’s contention also. Regulation can and should change behaviour, but it cannot alone change culture. A positive culture requires new ways of acting, must be led from the top and be seen as integral to good corporate governance. We in the IBCB have been working on facilitating an environment where ethical conduct at both personal and organisational level is encouraged and enhanced to the extent that it becomes inevitable. Examples of this approach may be seen in our DECIDE framework for ethical decision making and the recently launched Guiding Principles for Change agreed by all our five member banks. These two initiatives are good examples of the banks themselves pursuing and supporting positive cultural change. Details of these two initiatives may be found on our website.

The proposed scheme for individual accountability will surely attract and deserves to attract great interest and debate in the coming months. The senior executive accountability regime contained within the scheme is something worthy of close study and, as I stated above, we intend to participate and contribute to that effort.

Studies so far, so well outlined and analysed in this book and clearly articulated at our 2021 roundtable, show that the Individual Accountability regime, far from being something for the industry to fear or resist is in fact a new business model that can be of great assistance in the efficient management of modern companies including banks. The clear identification of roles and responsibilities inherent in the system has been found to be a welcome part of the corporate structures involved. Drawing from our initial roundtable, it is apparent that, for example in the UK, the need for enforcement has been minimal because of the close cooperation between the regulator and regulated entities. It is greatly to be hoped that the system when introduced in Ireland will follow that same course. A move in this direction will be an indication of a maturing environment for financial services in Ireland, characterised by mutual respect between the regulator and the regulated. I hope that this may contribute to a more balanced discourse on banking and assist with ensuring that the industry continues to be attractive for top tier talent.

The authors argue for a professionalizing of the banking sector. In this they foresee a more effective and sustainable way of ensuring that business is conducted in an ethical manner. I note in this regard that the Institute of Banking is well established in this context and delivers a range of internationally recognised accreditations and qualifications designed to equip the sector for developments and changes in the industry. The IBCB strongly supports the Institute’s qualifications in ethics, culture and conduct in particular and considers them an important means of embedding ethics in the day-to-day business of financial services.

END

Closing Remarks

It has been a very difficult few years for all involved in the banking sector in Ireland. Starting with customers and including bank staff at all levels, SMEs, farmers, senior customers, customers in vulnerable situations – the board community in general.

Our role to which we are totally committed is to work with the banks and all of the sector to build trustworthiness and thus regain the public trust. I want to take this opportunity to observe after three years of our Board’s existence, that all in the industry who we have encountered have worked closely and well with us in this endeavour.

The banking industry is a vital part of our society and economy as are all those who work within it. Ireland needs a robust and trusted banking sector and I believe that we are well on the way to achieving that essential goal.

I see this forthcoming individual accountability framework as an opportunity for everyone directly involved to work closely together so that trust can be built up again. As this book demonstrates, that is how the individual accountability framework is working in the other countries studied – I hope and I believe that is how it will work in Ireland.

I will close with the three words that should close every book launch – buy the book!